Good afternoon.

This is not the first time I have encountered such a problem in standard 1C 3.0 configurations when calculating wages. In this case, we are talking about both 1C Salary and HR Management 3.0 and 1C Enterprise Accounting 3.0. In 1C, when calculating wages, the amount “Excessively withheld personal income tax” appears on the payroll or payslip. Where did she come from? Where can I watch it? How can I remove it, at least with my hands? How can I stop it from appearing again?

The worst thing is that it affects the amount to be paid to the employee. In most cases, the amount of excessively withheld personal income tax is equal to the personal income tax accrued in the current month, although divergences are possible.

This article will not discuss when excessively withheld personal income tax actually occurs; I will talk about the most common case when it appears in the program, but it should not exist. In editions 3.0, this error is very easy to achieve and it is not immediately clear what to do about it.

So, today I suggest you deal with this problem. I hope many will thank me)) Don’t skimp on your comments, registration takes 5 seconds, I don’t send spam to my visitors

Let's start in order. The first thing I want to tell you is methodology for calculating excessively withheld personal income tax and the reasons for its incorrect appearance.

As you know, in personal income tax cards there is such a thing as “Personal income tax accrued” and “Personal income tax paid”; in practice they are almost always equal, but in theory they can diverge. For example, if the employee was not paid the accrued amount. So, if this is possible, then 1C should keep records of such situations, and they do. For accounting purposes, the accumulation register is used " Calculations of taxpayers with the budget for personal income tax". Accrual documents make the “receipt” movement in it, and payment statements make the “expense” movement.

In this case, personal income tax is taken into account as is known on an accrual basis. Those. the program analyzes all movements since the beginning of the year by the end of this month(verified 100% watched requests). Accordingly, if more was previously paid for an employee than accrued (well, you never know), then the employee must pay these amounts in person. For example, for the entire year, we accrued 3,900 rubles in personal income tax and paid 4,000 rubles, which means that when calculating the current month, we must pay the person 100 rubles more in person.

Now about the cause of the error: You calculated the salary, verified everything and you liked everything, create a payment slip, and post it. In our accumulation register “Calculations of taxpayers with the budget for personal income tax” there is an income made by the document “Payroll” and an expense made by the document “Statement to the Bank”. The amounts of income and expenses are equal, everything is beautiful. After this, you recalculate your salary for some reason without posting the payroll.. You don’t even have to refill the accruals; you just need to adjust the amount manually, and the personal income tax will be recalculated automatically. When calculating, the accrual document ignores its own movements, this is correct, but it sees the movements of our statement. As a result, we have paid personal income tax without accrual, expenses without income. And this amount falls into " Excessively withheld personal income tax".

Now where to see it: You will most likely see this only in the report, or you will notice that after refilling the statement, the payment amounts have increased. The fact is that by default, in 1C Enterprise Accounting 3.0, in 1C Salary and Personnel Management 3.0, the field where this amount is stored is hidden in all documents.

First, let's do the following: in the accrual document form, click the "all actions" button. Next, select “Change shape” from the drop-down menu. Here, if you have activated a plate with personal income tax data in the form, then you will immediately see “tax to offset refund”. Place a checkmark next to it.

Voila, we have found the enemy. At least we see it. Thank heavens, if the program is completed correctly, this setting will be saved and will not need to be done again. Now the enemy is always visible and you can always detect him in advance.

This field is present in all accrual documents where personal income tax is immediately calculated. In Accounting this is one document, but in ZUP there are a bunch of them.

Now How to fix it: not everything is so simple here, even in the ZUP it is intended that personal income tax is calculated on its own and its manual adjustment is not convenient. You can poke the amount twice, but before allowing you to edit it, the program will make sure you are sane by asking a stupid question. And so on for each line. Not only will she ask, but she will mark the corrected lines as manually edited (highlighted in bold), which can affect the auto recalculation when editing accruals. but 1C didn’t leave us any other way.

Now how to prevent this?: it’s very simple (probably) - post the statements before editing the accruals.

In small offices this is enough, but in large ones, where I calculate the salaries of several people at the same time, this is not suitable. Usually I use a simple processing that analyzes the presence of “Excessively withheld personal income tax”, finds the documents that generated it, edits the tabular part of the “personal income tax” accrual document, and resets the amounts in the column " tax to offset refund"and forwards the document. The advantage is that it does not enable manual adjustments in the lines. There is no need to poke at every line of the document. She will not miss a single document.

The processing is easy to use; it has a “report only” checkbox and period selection fields. When the "only report" checkbox is selected, processing does nothing, only reports the names of documents, if any. Those. it can also be used as a test.

If you want to integrate it into the database, then modify it according to the instructions in the article Creating external processing for managed forms. Simple processing, with the possibility of registration in additional reports and processing.

Thank you for your attention, see you soon. Write reviews.

Hello dear blog readers. We started a detailed conversation about personal income tax accounting in 1C ZUP and looked at the simplest example, which presented the full cycle of personal income tax accounting (by the way, you can read about the formation of 6-personal income tax in the article). In that example, personal income tax was calculated using the “Payroll” document. Today I will tell you in what other documents it is possible to calculate personal income tax, and we will also talk about what parameters are available in the 1C Salary and Personnel Management program for setting up personal income tax accounting, why they are needed and where they are located. In particular, we will discuss personal income tax deduction settings, as well as possible options for choosing the status of an individual for personal income tax accounting purposes ( resident, non-resident, highly qualified foreign specialist and others). In this article we will look at two examples:

- In the first one, we will work with the deduction settings - the employee has 4 deductions;

- In the second example, let's see how the program reflects and compensates for excessively withheld personal income tax when the taxpayer's status changes.

✅

✅

So, in the previous publication an example was presented where an employee had only one planned type of accrual, which was calculated in the document "Payroll" and personal income tax from this accrual was also calculated in the same document. But in 1C ZUP there are also a number of accrual documents that provide for the calculation of personal income tax. Let me first list all these documents:

- – “Payment” tab;

- – tab “Calculation of sick leave” -> “Personal income tax”

- – “NDFL” tab

The ability to calculate personal income tax in these documents appeared not so long ago. Previously, personal income tax was calculated only in document "Payroll" and that's why it should have been a last resort so that all accruals for the month are taken into account to correctly calculate personal income tax. This recommendation should still be followed now. Since most of the accrual documents still do not support the independent calculation of personal income tax, the amounts for these documents will be taken into account when calculating personal income tax in the final document “Payroll.” These include the following documents:

- Employee bonuses;

- Registration of downtime of employees of organizations;

- Calculation of severance.

Setting up personal income tax deductions in 1C ZUP

✅

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

Now let's talk about how the program sets up accounting for standard tax deductions. First, let me remind you what a tax deduction is. A tax deduction is a certain amount that reduces the tax base, i.e. not subject to personal income tax. In essence, this is a benefit established by the state for a certain circle of citizens. This is where I started talking about standard tax deductions. These include:

- 1400 rub. – for each child (for the first and second child) – code 114/108 (for the first child) and code 115 (for the second child);

- 3000 rub. – for the third and each subsequent child – code 116;

- 3000 rub. – for each disabled child of group I or II – code 117/109;

- 500 rub. - for persons with state awards: in particular, for Heroes of the Soviet Union, Heroes of Russia, for those awarded the Order of Glory of three degrees and many others - code 104 (in the ZUP this deduction is considered a personal standard deduction);

For those who are just starting to get acquainted with the theory of payroll calculation, accounting for personal income tax and deductions, I will give a small example. Let's assume that employee Stepanova has four children, i.e. she has the right to 2 deductions of 1400 rubles each. (code 114 and 115) and 2 deductions of 3000 rubles each. for the third and fourth child (code 116). She also has a salary of 30,000 rubles. Under these conditions, personal income tax (13%) will be calculated using the following formula: (30,000 – (1,400 + 1,400 + 3,000 + 3,000)) * 13% = 21 200 * 13% = 2,756 rub. Thus, the tax base will not be the entire salary, but the amount reduced by the amount of deductions due.

Let's now implement this example in the 1C ZUP program. To fill out information about an employee’s right to standard deductions, the program uses the “Data Entry for Personal Income Tax” form. It can be accessed from the “Employees of the Organization” directory form.

You can also fill in the Reason field, but this is not required. If the Deduction is terminated, the Date and status are indicated "do not apply".

In our example, the employee does not have personal deductions, so we will leave this tabular part empty.

The second tabular part in this form is called "Eligibility for Standard Deduction for Children". We will fill out this form for employee Stepanova. Let me remind you that, according to the conditions of the example, she has four children and, accordingly, can use the following deductions:

- 114/108 – for the first child 1,400 rubles;

- 115 – for the second child 1,400 rubles;

- 116 – for the third and fourth child, 3,000 rubles each. for everyone;

The fields in this tabular section are approximately the same. The only difference is that you can indicate the number of children (we use this option for deduction code 116) and indicate the date until which the deduction is valid, if this is known in advance (we use this for deduction 114/108). You can also stop deduction by entering a separate line, indicating the value “Do not apply”, deduction code and date. The screenshots show both options.

Another tabular part in this form is called "Application of deduction".

And this you need to do it even if you have one organization in the program, otherwise deductions will not be taken into account.

I would also like to draw your attention to the fact that there is another bookmark in this form. Let me remind you that the standard tax deduction is applied until the employee’s cumulative income from the beginning of the year does not exceed 280,000 rubles. Therefore, if an employee does not join the organization from the beginning of the year, then for him you should indicate the income that he had in the previous or previous organization from the beginning of the year. This data will only be taken into account to track the RUB 280,000 limit. These amounts will not affect the calculation of average earnings in any way.

In our case, the employee was hired at the beginning of the year and therefore bookmark “Income from previous jobs” leave it blank.

Taxpayer status for personal income tax

✅ Seminar “Lifehacks for 1C ZUP 3.1”

Analysis of 15 life hacks for accounting in 1C ZUP 3.1:

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

Taxpayer status in 1C ZUP can be established using the form “Data entry for personal income tax”. It can be opened from the form of the “Employees” directory element in the “Status” field. There are 5 options to select the status:

- Resident

- Non-resident

- Highly qualified foreign specialist

- Participant in the program for the resettlement of compatriots

- Refugee or who has received temporary asylum on the territory of the Russian Federation - appeared in the release of ZUP 2.5.85

There are explanations in the program for each option, so I will only focus on the features of reflecting the situation when an employee’s status changes in the middle of the year. As you can see, in addition to the switches themselves, the form has a field where the period is set. Those. this indicator is periodic. Let's look at a similar situation.

An employee who is a foreign citizen and at the time of hiring (01/10/2014) resides in the Russian Federation is hired by the organization. less than 183 calendar days. Therefore, he is given the status "Non-resident". As a result, personal income tax for January and February is calculated at a rate of 30%.

It turns out that the employee’s personal income tax for January and February is 18,000 = 9,000 + 9,000 = 30,000 * 30% + 30,000 * 30%.

In March, the deadline comes when a foreign citizen’s stay on the territory of the Russian Federation will exceed 183 days. Therefore he acquires the status "Resident". In this case, in 1C it is necessary to change the employee’s status indicating the month in which he received the corresponding status and this will be saved in the history of changes.

As a result, the employee’s personal income tax will begin to be calculated at a rate of 13% from March. But this is not the only change that will occur. When calculating personal income tax for March, the tax for January and February will be recalculated at a rate of 13%. Negative amounts will be calculated for January and February: 30,000 * (13%-30%) = -30,000 * 17% = - 5100; -5,100 *2 = -10,200 rub. (excess withheld for 2 months).

Refunds of excess withheld amounts will be made from the tax calculated in March: RUB 3,900. Those. in March, the employee will receive his full salary without personal income tax withholding. However, personal income tax for March is not enough to fully compensate for the excessively withheld amount and therefore in the pay slip for March in the line “including: excessively withheld personal income tax at the end of the period” we will see the figure 6,300 = 10,200 (the amount of excess withheld at the beginning of March) - 3,900 (returned from the March personal income tax).

Please note that this debt in the amount of 6,300 rubles. Although it is listed as a debt for the organization, it will not affect the amount of salary payable. The employee will be paid 30,000, not 36,300.

Thus, the return of excessively withheld personal income tax to the employee will be carried out in the next two months, at the expense of the calculated personal income tax in these months. I hope I explained this mechanism clearly.

In this example, we have a rather simple situation: the employee’s status changed at the beginning of the year and there is time to compensate for personal income tax due to the following months. But it may turn out that the employee changes status, for example, in November and simply there won't be enough time until the end of the year to compensate the entire excess amount withheld. In this case, the program will not carry over this debt to the next year. The employee should independently contact the tax office and it will be the one who will return the excess withheld funds to him. In this case, you should not enter the document "Personal income tax return", since the tax agent (the employer is the tax agent for the payment of personal income tax) does not have the right to return personal income tax to the employee, but can only offset the overpaid amounts against the following months (I talked about this a little higher with an example).

That's all for today!

To be the first to know about new publications, subscribe to my blog updates:

The procedure for collecting and returning personal income tax is regulated by Article 231 of the Tax Code of the Russian Federation. Taxpayers have many questions, so we will dwell on the most common cases, and also give recommendations on how to reflect actions for recalculation, collection and return of personal income tax in the programs of the 1C: Enterprise 8 system.

Additional tax assessment

The current rules for collecting personal income tax have not changed. Consequently, if for some reason the tax agent did not withhold personal income tax from the income of an individual or did not withhold the tax in full, then the missing amounts must be recovered from the taxpayer. Tax may be under withheld for the following reasons:

- by mistake if you provided an extra deduction or incorrectly indicated the income code;

- there was a recalculation for the previous period, and income increased;

- the individual has lost his tax resident status.

If the employee continues to work and receive income, then after correcting the error, recalculation or change of status, during the next personal income tax calculation in the accounting programs of the 1C: Enterprise 8 system, the missing amount will be automatically calculated and withheld.

If non-payment of tax is discovered when there is no way to withhold the tax (if the employee quits or the tax period has ended), then the organization will not be able to collect personal income tax. Paragraph 5 of Article 226 of the Tax Code of the Russian Federation states that if it is impossible to withhold from the taxpayer the calculated amount of personal income tax, the tax agent is obliged to inform the taxpayer and the tax authority at the place of his registration in writing about this and the amount of tax using a certificate of form 2-NDFL, approved by order of the Federal Tax Service of Russia dated 11/17/2010 No. ММВ-7-3/611@.

To do this, you need to generate a 2-NDFL certificate in the program in paper or electronic form and send it to the taxpayer and the tax authority at your place of registration. For 2011 cases, this must be completed no later than January 31, 2012.

Personal income tax refund

Tax may be overcharged for the same reasons as undercharged.

The general procedure for the return and offset of overpaid and collected taxes is established by 79 of the Tax Code of the Russian Federation. The new version of paragraph 1 of Article 231 of the Tax Code of the Russian Federation (came into force on January 1, 2011) clarified the rules for the return of personal income tax to an individual from whom the tax agent, for any reason, withheld excessive tax.

If the reason for over-withheld tax is a changed state of deductions or income, then from the beginning of the current year the tax agent is obliged to inform the individual from whom he previously over-withheld tax about each such fact within 10 business days from the day the agent became aware of it. In this case, the excessively withheld amount of personal income tax is indicated. The form of the message is not regulated and can be arbitrary.

The amount of tax withheld in excess is subject to refund based on a written application from the taxpayer (paragraph 1 of Article 231 of the Tax Code of the Russian Federation). Therefore, we recommend that tax agents (employers) include a phrase in their message about the need to write such a statement. It should also be noted that the refund of the overly withheld tax amount to the taxpayer is possible only in non-cash form. Therefore, the taxpayer’s application must indicate the bank account to which the funds due to him should be transferred.

The message can be given to the taxpayer or sent by mail.

The requirement that appeared last year in the Tax Code of the Russian Federation to promptly inform the taxpayer about the existing overpayment of tax is not accompanied by regulations for recording the fact of detection of excessive withholding of personal income tax from the taxpayer’s income. The liability of the tax agent for failure to inform the taxpayer is also not provided for.

Having received an application from the taxpayer for the return of the excessively withheld amount of personal income tax, the employer decides from what funds it will be returned. The refund is possible at the expense of personal income tax amounts subject to transfer to the budget system of the Russian Federation on account of upcoming payments both for this taxpayer and for other taxpayers from whose income the agent withholds tax (paragraph 3, clause 1, article 231 of the Tax Code of the Russian Federation). The method for making a refund is selected based on the amount of tax being refunded and the deadline set for its refund. The agent must return the tax to the taxpayer within three months from the date of receipt of the relevant application from the taxpayer. Since the beginning of this year, the tax agent has been legally granted the right to refund overpaid tax at his own expense, without waiting for funds to be received from the tax authority (paragraph 9, clause 1, article 231 of the Tax Code of the Russian Federation). However, the Russian Ministry of Finance has repeatedly reminded (letters from the Russian Ministry of Finance dated May 11, 2010 No. 03-04-06/9-94, dated August 25, 2009 No. 03-04-06-01/222) that it is necessary to refund personal income tax only at the expense of tax amounts , withheld from payments of this individual.

In order to return personal income tax in 1C:Enterprise 8, you need to enter a document into the database Personal income tax return: Desktop of the program “1C: ZUP 8”-> bookmark Taxes and fees -> Personal income tax refund(Fig. 1).

Rice. 1

Based on the submitted document, money should be transferred: Menu Action -> Based on -> Salary to be paid(Fig. 2).

Rice. 2

But please note that there is no liability for failure to inform about over-withheld tax. In addition, an informed employee is not obliged to insist on the return of personal income tax. That is, if the employee continues to work and has not submitted an application for a tax refund, then during the next personal income tax calculations in the 1C:Enterprise 8 programs, the excess accrued amount will automatically be taken into account when calculating personal income tax. The Tax Code of the Russian Federation does not prohibit the continuation of offset of over-withheld tax in the next tax period. For example, an employee overpaid personal income tax was discovered in December. This situation will occur in 2011 for employees who have a third child or a disabled child. Let us recall that Federal Law No. 330-FZ of November 21, 2011 increased standard deductions for personal income tax for children retroactively, i.e., from January 1, 2011.

If employees submit applications and provide documents stating that the child is disabled or the third in the family, it will be necessary to enter information about these deductions from 01/01/2011 (Fig. 3). Take advantage Assistant for editing deductions for children, to facilitate the replacement of deductions for third and subsequent children. Commands for calling the Assistant on the Desktop of the 1C: Salaries and Personnel Management 8 program -> tab Taxes -> Editing deductions for children and in the menu Taxes and fees.

Rice. 3

If a deduction for a disabled child has already been established, its amount will change automatically. These employees will be overpaid in taxes. Employees may not have time or may not want to submit an application for a personal income tax refund. When submitting the 2-NDFL report to the Federal Tax Service, the tax agent will indicate the amount of the overpayment there. The taxpayer may not apply to the Federal Tax Service for a tax refund. A tax agent - an organization - can continue to count overpayment amounts when making calculations in 2012. This approach is implemented in the 1C:Enterprise 8 programs.

If an overpayment of personal income tax is detected when the employee no longer works for the organization, then the tax agent reports the overpayment of tax at the end of the tax period in the 2-NDFL report to the tax authority and notifies the taxpayer about this, and the taxpayer must receive a refund of the over-withheld amounts. contact the tax office at your place of residence.

Recalculation of taxes when acquiring Russian resident status

An excessively withheld amount of personal income tax also arises in the event of a change in the status of the taxpayer from a non-resident to a resident of the Russian Federation. A non-resident paid personal income tax at a rate of 30%. After an individual is recognized as a tax resident of the Russian Federation, the specified income in accordance with paragraph 1 of Article 224 of the Tax Code of the Russian Federation is subject to taxation at a rate of 13%.

Until 2011, such overpayments were subject to refund. Legislative changes have confused users. The prohibition on the return of overpayment of personal income tax that arose in connection with a change in the taxpayer’s status does not mean that it is not necessary to recalculate the tax at a rate of 13% and take into account the overpayment in the next assessments.

Letters from the Ministry of Finance of Russia dated 08/12/2011 No. 03-04-08/4-146 and the Federal Tax Service of Russia dated 06/09/2011 No. ED-4-3/9150 indicate that the tax agent calculates, withholds and pays personal income tax amounts to the budget system of the Russian Federation with taking into account the tax status of the taxpayer determined on each date of payment of income. Having determined at a certain date the change in the status of a non-resident to the status of a resident, when calculating personal income tax, it takes into account the amounts that were previously accrued at a rate of 30%.

Users of 1C:Enterprise 8 programs do not need to do anything in this case. It is enough to indicate only the change in taxpayer status and the recalculation will be made automatically when calculating personal income tax.

Letter of the Ministry of Finance of Russia dated November 22, 2010 No. 03-04-06/6-273 indicates two cases in which tax refunds can only be made to the Federal Tax Service: change of Russian resident status, property deduction.

If an employee applies to an employer for a property tax deduction not from the first month of the tax period, the deduction is provided starting from the month of application.

A refund of over-withheld tax can be made by the tax authority when the taxpayer submits a tax return to the inspectorate based on the results of the tax period.

The Ministry of Finance repeatedly indicates in its letters that those amounts of tax that were withheld in accordance with the established procedure before receiving the taxpayer’s application for a property tax deduction and the corresponding confirmation from the tax authority are not “excessively withheld.”

However, representatives of the Federal Tax Service of Russia in a letter dated 06/09/2011 No. ED-4-3/9150 indicate that the refund of over-withheld tax when changing the status of a resident of the Russian Federation can be carried out by the tax agent-employer during this tax period.

In a letter from the Ministry of Finance of Russia dated September 28, 2011 N 03-04-06/6-242, Deputy Director of the Department of Tax and Customs Tariff Policy S.V. Razgulin replies that the above letter from the Federal Tax Service is a request to the Ministry of Finance of Russia, to which there were appropriate explanations were given. And the letter of the Ministry of Finance dated August 12, 2011 No. 03-04-08/4-146, which was issued in response to a request from the Federal Tax Service, clearly indicates that in accordance with paragraph 1.1 of Article 231 of the Tax Code of the Russian Federation, the provisions of which came into force on January 1, 2011. , the refund of the amount of personal income tax to the taxpayer in accordance with the status of a resident of the Russian Federation acquired by him is carried out by the tax authority with which he was registered at the place of residence (place of stay). The refund is made when the taxpayer submits a tax return at the end of the specified tax period, as well as documents confirming the status of a tax resident of the Russian Federation in this tax period, in the manner established by Article 78 of the Tax Code of the Russian Federation.

Thus, if an employee of an organization acquires the status of a tax resident of the Russian Federation, the tax amount is refunded based on the results of the tax period by the tax authority.

Users of the 1C:Enterprise 8 programs only need to indicate the date of change of taxpayer status and the recalculation will be made automatically when calculating personal income tax.

ATTENTION: similar article on 1C ZUP 2.5 -

Hello dear site visitors. Today in the next article we will talk about how in the program 1C 8.3 ZUP 3.1 The process of accounting for various types of personal income tax has been organized:

- Calculated personal income tax

- Withheld personal income tax

- Listed personal income tax

We will look in detail at what documents these types of personal income tax are taken into account and in what registers they are reflected. Let's look at a specific example of how to register in a program employee's right to receive a standard tax deduction and how it will be taken into account when calculating personal income tax. Let's consider some other settings that must be taken into account for the correct calculation of personal income tax in the 1C ZUP program, edition 3.

✅

✅

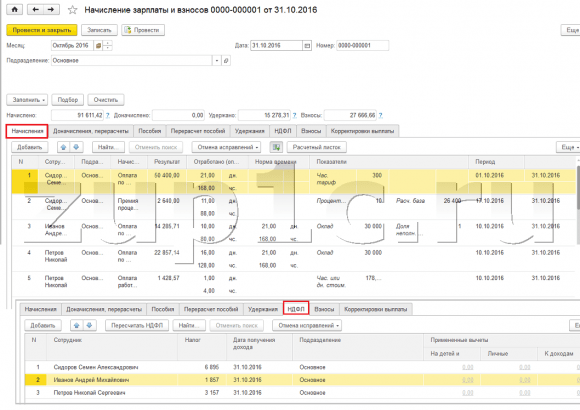

First we'll talk about calculated personal income tax. In the ZUP 3.0 (3.1) program, this personal income tax is calculated in the documents “Accrual of salaries and contributions”, as well as in various inter-account documents, such as “Vacation”, “Business trip”, “Sick leave”, “Bonuses”, “One-time accruals” and in some others. First, let's talk about how it is calculated Personal income tax in interpayment documents. I will analyze today’s material on the basis of the information base that we have formed as a result of previous publications, where I talked about and.

Let's look at the inter-account document “Sick leave” for employee A.M. Ivanov. for October. This document is a personnel accounting document and when filled out, the program automatically determines the employee’s average earnings for the two calendar years preceding the year of temporary disability. Here, sick leave is completely calculated based on average earnings, and calculated by personal income tax. You can view the details of the calculation of this tax by clicking on the button with the image of a green pencil.

In the window that opens “More details about personal income tax calculation” we will see the amount of calculated tax, date of receipt of income, for which it is calculated, possible standard and property deductions, if they are registered for the employee. In our example, Ivanov A.M. There are currently no personal income tax deductions. Personal income tax was calculated correctly - 252 rubles, which is 13% of the amount of income of 1,935.49 rubles.

I would like to pay special attention to the props "payment date" in the document “Sick leave”. The fact is that it is very important to correctly indicate this date in interpayment documents. For incomes for which the income code is NOT equal to code 2000 or 2530 (and for hospital income code 2300), it is according to "payment date" determined "date of receipt of income", and this date determines which month of the tax period the income and the personal income tax calculated from it will be attributed to.

In the document “Sick leave” the date of payment is indicated 05.11 (payment with salary) and based on it was automatically filled in date of receipt of income Also 05.11 , which is what we actually see in the “More details about personal income tax calculation” window. Accordingly, we will have the month of the tax period for personal income tax accounting purposes November. Where can we see this period? For example, if according to employee Ivanov A.M. generate a “Certificate of Income (2-NDFL)”, it will be seen that income with code 2300 (and these are sick leave, in the amount of 1,935.49 rubles for our example) fell in the month of the tax period November. The same thing will happen in the regulated report “2-NDFL for transfer to the Federal Tax Service” if we generate it.

It should also be said that the date of receipt of income, which will be determined for the calculated personal income tax in the intersettlement document, directly affects the completion of the quarterly 6-personal income tax report. I discuss the issue of filling out 6-NDFL in 1C ZUP 3.0 (3.1) in great detail in the article

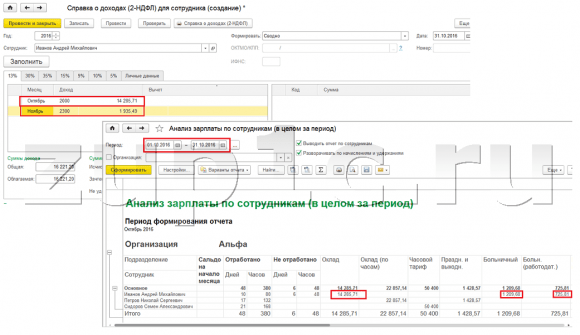

So this sick leave in tax accounting was registered in November. We are convinced of this. But it is worth noting that the accrual month in the “Sick Leave” document is indicated as October. This means that if we generate salary reports in the program from the Salary (Salary Reports) section, such as “Payslip”, “Full set of accruals, deductions and payments” or “Salary analysis for employees (as a whole for the period)” , then in them this sick leave will be attributed to the month October. Let's look at the example of Salary Analysis for Employees, indicate the period from 01.10 to 31.10 and see that sick leave is included in the report.

Those. there is a difference between what month of the tax period this income is registered (NOVEMBER), and to which month of accrual, he is assigned (OCTOBER). It is worth understanding this difference and keeping in mind that this situation is normal.

Registration of calculated personal income tax with the document “Accrual of salaries and contributions” in 1C ZUP 3.1 (3.0)

Now let's look at the document "Calculation of salaries and contributions" for October. Here, personal income tax is also calculated (the “personal income tax” tab), and the screen below shows that in this example, personal income tax is calculated exactly from the employee income that is accrued in this document. But in fact, the program analyzes all employee income from the beginning of the year, i.e. Personal income tax is calculated on an accrual basis from the beginning of the year. If the program sees that for some reason the tax was not calculated in interpayment documents or in previous months, but should have been, then this personal income tax will be calculated here, i.e. The program will not lose any income.

To illustrate this point, let’s remove the personal income tax in the Sick Leave document and assume that for some reason it was not calculated. Let's spend sick leave in this form.

Now, let’s recalculate personal income tax in the document “Calculation of salaries and contributions.”

Please note that according to employee Ivanov A.M. in the document “Calculation of salaries and contributions” on the personal income tax tab, we now have two lines formed. In the first line, 1857 rubles. - this is the calculated tax on salary payment in the amount of 14,285.71 rubles. The second line, 252 rubles, is the tax calculated from sick leave and we can determine this by the date of receipt of income 05.11, which corresponds to the date of payment in the “Sick Leave” document.

Thus, the date of receipt of income will be the last day of the month for which it was accrued, i.e. 31.10.

The same goes for other employees. Sidorov S.A. in October, payment was accrued at an hourly rate and a percentage bonus; these types of accrual also have an income code of 2000, respectively, the date of receipt of income is the last day of the month - 10/31.

Employee Petrov N.S. in October, payment was accrued based on salary (by the hour) and payment for work on holidays and weekends, these types of accrual also have an income code of 2000, respectively, the date of receipt of income is the last day of the month - 10/31

Thus, the date of receipt of income is determined in accordance with the income code specified in the accrual type settings. For income with code 2000.2530 “date of receipt of income” is defined as the last day of the month, for which income is accrued, and for other income - by date of payment of income.

For clarity, we will also create a “Vacation” document for employee S.A. Smirnov. If we look at the details of the calculation of this personal income tax, we will see that the “date of receipt of income” was also determined by the “date of payment” specified in the document - 07.11

Therefore, I would like to draw your attention once again to the fact that very important correctly indicate the date of payment of income in interpayment documents. In the document “Accrual of salaries and contributions”, the date of payment does not need to be indicated, since the program automatically determines the date of receipt of income based on the month for which income is accrued and sets the last day of this month.

Let's look again at the “Certificate of Income (2NDFL)” for employee A.M. Ivanov. Here we see that income code 2000 (salary payment) in the amount of 1,4285.71 rubles is assigned to the month of the tax period October, and income code 2300 (Sick leave) in the amount of 1,935.49 rubles - November. But in the salary report “Analysis of salaries by employees” for the period from 01.10 to 31.10, both Salary and Sick Leave are indicated.

I would also like to talk about the technical side of this issue, i.e. tell us in which registers in the 1C ZUP 3.0 (3.1) program it is taken into account counted Personal income tax (by the way, I have already discussed this issue in some detail in the article). So, in order for us to view these registers, it is enough to open the document “Accrual of salaries and contributions”, i.e. the document in which this personal income tax was calculated and directly into the form of this document display all those registers on which this document can make movements. To do this, open the Main menu – View – Setting up the form navigation panel. In the “Available commands” field, select the register we need, it is called “”, and it is taken into account counted Personal income tax, click the “Add” button and this register will go to the “Selected commands” field. Click OK.

A link will appear at the top of the “Payroll and Contributions” document “Calculations of taxpayers with the budget for personal income tax”, when opened, you can view the movement of this document in this register. In the register Calculations of taxpayers with the budget for personal income tax 4 entries occurred, exactly those that are present on the personal income tax tab in the “Calculation of salaries and contributions” document.

I want to draw your attention to the fact that this movement is done with a plus sign, that is incoming movement, and means that this counted Personal income tax. An expense movement with a minus sign in this register is withheld personal income tax. We'll talk about it further.

Registration of withheld personal income tax with the documents “Vedomost...” in 1C ZUP 3.1 (3.0)

✅

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

Firstly, it is worth noting that in the 1C ZUP 3.1 (3.0) program registration withheld personal income tax carried out in the documents “Vedomost...”:

- "Statement to the bank"

- “Statement of transfers to accounts”,

- "Statement to the cash register"

- “Payment sheet through the distributor.”

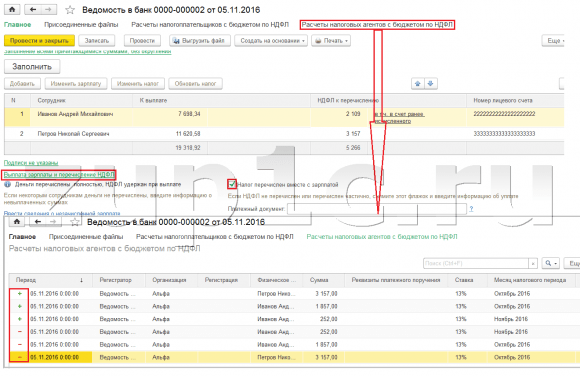

For our example, we will create the document “Statement to the Bank”. The program will automatically fill out the document with those employees whose payment method is assigned in the organization’s settings, i.e. by crediting to the card within the framework of a salary project (in our example, these are employees A.M. Ivanov and N.S. Petrov). You can read more about paying advances and salaries in 1C ZUP in the article.

When filling out this document, the program analyzes not only the balance of debt to the employee (the “Payable” column) and not only indicates the amount to be paid, but also fills out the “Personal Income Tax to be Transferred” column, i.e. the tax that will be withheld when processing the document. When filling out this column, the program analyzes the remainder by register “Calculations of taxpayers with the budget for personal income tax”, is there in this register counted, but also unrestrained tax. Therefore, if for some reason personal income tax for the previous months was not reflected as withheld, then the program will take it into account the next time you fill out the “Vedomost...” document.

Now let’s look in more detail at what it was made up of by employee A.M. Ivanov. To do this, double-click on the amount of 2,109 in the “Personal Income Tax to be transferred” column. The “Editing Employee Personal Income Tax” window will open, where we see personal income tax in the amount of 1,857 rubles. from income from salary (date of receipt of income 10/31) based on the document “Accrual of salaries and contributions” and personal income tax in the amount of 252 rubles from sick leave (date of receipt of income 05/11) based on the document “Sick Leave”.

Next, let’s see what movements the document “Statement to the Bank” will make according to the register. For ease of viewing, we will display a link to this register directly in the document form. In exactly the same way as we did in the document “Calculation of salaries and contributions” (Main menu - View – Setting up the form navigation panel). So let's follow the link “Calculations of taxpayers with the budget for personal income tax.” Now we see that, unlike the document “Calculation of salaries and contributions” (receipt movement with a plus sign), the document “Statement to the bank” does consumable movement with a minus sign. It is the expense movement in this register that reflects the fact withholding personal income tax.

Here it is immediately worth noting that it is precisely based on the expense movements of this register that section 2 in the report “6 Personal Income Tax” is formed (more details in the article). And in this regard very important so that the retention period (date) is indicated correctly. In fact, this is line 110 in section 2 of the “6 personal income tax” report. The retention date (period) in the register is filled in automatically in accordance with the date specified in the “Statement...” document. Therefore, once again I draw your attention, very important To correctly fill out section 2 of report 6 of personal income tax, correctly indicate the date in the document “Statement...”, i.e. exactly the date when wages are actually paid and personal income tax is withheld accordingly.

Registration of the listed personal income tax with the documents “Vedomost...” in 1C ZUP 3.1 (3.0)

✅ Seminar “Lifehacks for 1C ZUP 3.1”

Analysis of 15 life hacks for accounting in 1C ZUP 3.1:

✅ CHECKLIST for checking payroll calculations in 1C ZUP 3.1

VIDEO - monthly self-check of accounting:

✅ Payroll calculation in 1C ZUP 3.1

Step-by-step instructions for beginners:

In the 1C program ZUP 3.1 (3.0) personal income tax listed, as well as withheld, are registered by default in the “Vedomost...” documents. Let's look at the listed tax using the example of the document “Statement to the Bank”. If we follow the link Payment of salaries and transfer of personal income tax, which is located at the bottom of the document, then some more details of this document will open. By default, this checkbox is checked Tax is transferred with salary and that is why the document “Gazette …” registers the fact of personal income tax transfer. In the payment document field, we can immediately indicate the number and date of the payment document by which the personal income tax was transferred.

Now let's talk about registers. Listed personal income tax reflected in the register. Let's display a link to the register Calculations of tax agents with the personal income tax budget to the form of the document Statement to the Bank (Main menu – View – Setting up the form navigation panel) and see its contents. In this register income movement with plus now registers fact retention Personal income tax, and with a minus - consumable movement registers listed tax.

Now let's talk about an alternative way of registering the fact of transferring personal income tax to the budget. If we do not want to reflect the fact of personal income tax transfer in the “Vedomosti...” document itself, then the program contains a document “Transfer of personal income tax to the budget”. But why might we not want this?

In this situation, if we reflect the transfer of personal income tax in the document “Sheet ...”, then in fact in the program this transfer is registered on the date that appears in the Sheet itself, i.e. in our example, the fact of transfer was registered on the date 05.11. If we actually transferred this personal income tax the next day, i.e. 6.11 (we have the right to transfer personal income tax no later than the next day after payment of wages, and personal income tax from sick leave and vacation pay no later than the end of the month), and not 5.11, then it turns out that we store not entirely reliable information in the program. Therefore, for more correct accounting, this listing should be reflected in 6.11.

But, nevertheless, I will show how to reflect the transfer of tax in a document “Transfer of personal income tax to the budget”.

Let’s uncheck the checkbox in the “Statement to the Bank” document “The tax is transferred along with the salary” and we will make a statement. Let's follow the link Calculation of tax agents with the personal income tax budget and we will see that now the document only does income movement with a plus sign, i.e. registers only held Personal income tax, but the one listed was not recorded.

Next, please note that a new link has appeared in the document “Statement to the Bank” Enter personal income tax transfer data. Let's use it, and the program will transfer us to the document log Transfer of personal income tax to the budget. Let's create a new document. We will transfer the tax on 06.11. In the Amount field, we will enter the amount of tax that is indicated in the document Statement to the bank in the column “Personal income tax to be transferred” in the amount of 5,266 rubles, i.e. We will remit any tax withheld on this statement. Click the spend button.

The program begins to analyze the register Calculations of taxpayers with the budget for personal income tax in the document “Statement to the Bank”. She sees that there is an incoming movement of the withheld tax, but there is no outgoing movement of the transferred tax. That is, there is a remainder in this register. The amount of 5,266 rubles is distributed in proportions between all these balances (by Employee and Date of receipt of income) and is formed consumable movement, i.e. fact of personal income tax transfer. Accordingly, we list what is withheld. You can compare. Let's open the register Calculations of taxpayers with the budget for personal income tax in the document “Statement to the Bank” and in the document “Transfer of personal income tax to the budget”. That's right, all the tax has now been transferred to us.

So, we've run out of lengthy questions. We have sorted out which documents are in the program 1C ZUP 3.0 (3.1) registered calculated, withheld and transferred tax, as well as in which registers these taxes are recorded. Now we will talk about tax deductions for personal income tax. We considered the examples given above without taking into account tax deductions.

Registration of an employee’s right to provide a standard tax deduction in the 1C ZUP 3.1 (3.0) program

The tax base is determined as the amount of income minus the amount of tax deductions provided. There are five types of tax deductions:

- Standard

- Property

- Professional

- Social

- For partially taxable income

In today's article we will talk about how to register an employee's right to provide a standard deduction in the program. Let’s go to the “Taxes and Contributions” section in the “Application for Deductions” journal. Let's open it, here we can create documents such as an application for deductions for personal income tax, Cancellation of standard deductions for personal income tax, Notification of non-commercial organizations about the right to deductions. Let's create a document “Application for personal income tax deductions”. The deduction is provided to employee Petrov N.S., we indicate the date of the document - 01.11, the month from which this deduction will be applied November. Click the “Add” button and from the list of types of personal income tax deductions proposed by the program, select deduction with code 114 (for the first child under the age of 18, for a full-time student, graduate student, resident, student, cadet, under the age of 24). We indicate the month until which the deduction is provided - December. We carry out the document.

Also in the program, we can view information about the deductions provided directly in the employee’s card (section Personnel - Employees directory). Let’s open N.S. Petrov’s card. and follow the link "Income tax". A window will open where we will see the deduction provided to this employee, which we just entered in the document "Application for deductions." If we need to change something in the application, we can follow the link “Correct the application for standard deductions” directly from the employee’s card.

Now let's go to the link Income from previous place of work, In the tabular section, you should indicate the employee’s income from his previous place of work, if he has been working in our organization for more than a year and worked somewhere else this year. This information is necessary for the program to track excess income for the year for the purposes of accounting for deductions, i.e. stopped providing the deduction in a timely manner if the income was exceeded.

Also in this window there is a field where the taxpayer status is indicated. I did not mention this right away in order to present material about where and how various types of personal income tax are registered and proceeded from the fact that all our employees have taxpayer status - Resident(13%, personal income tax is considered a cumulative total). However, the program supports personal income tax accounting for employees with other taxpayer statuses, such as non-residents, highly qualified foreign specialists and others. And this status is selected for the employee here. Depending on the selected status, the tax rate and the algorithm for calculating personal income tax are determined. But this is a topic for other publications.

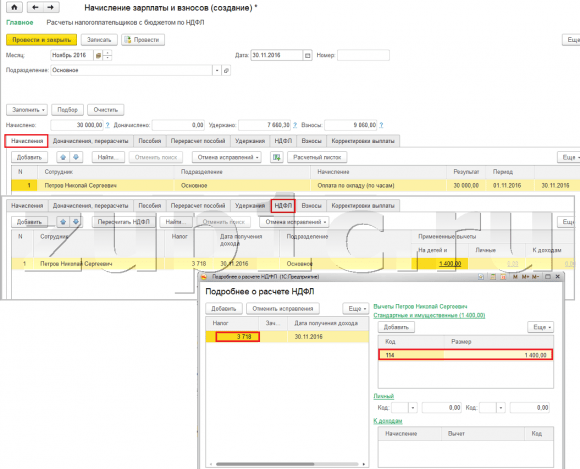

So, all the necessary information in the program for providing a tax deduction to employee N.S. Petrov. we have contributed, and now we just have to see how it will be taken into account when calculating personal income tax. We will generate a document “Calculation of salaries and contributions” for November. The employee is paid a salary of 30,000 rubles; on the personal income tax tab we see the calculated tax in the amount of 3,718 rubles, taking into account the applied deduction of 1,400 rubles. The calculation will be as follows: (30,000 - 1,400)*0.13 = 3,718 rubles.

In today's article we reviewed quite a lot of material. We talked about where and how to register calculated, withheld and transferred personal income tax. We looked at what tax deductions are provided to employees. Using a specific example, we registered an employee’s right to provide a standard tax deduction.

In the next article I will talk in detail about how contributions are taken into account in 1C ZUP 3.0 (3.1). Follow the publications. All the best!)