Economists and marketers, when analyzing any market, use a large number of various indicators. In order to be able to predict fluctuations in transaction volumes, the price elasticity of supply and demand is examined.

Having learned the level of these indicators, it becomes possible to make objective assessment the influence of price on the number of transactions carried out in a particular market. This article will discuss price elasticity of demand, formula, types and factors that can influence it.

Definition and essence

In textbooks on economic theory, an entire section is devoted to the issue of elasticity. This suggests that the topic is relevant and needs to be understood by people who want to become good economists or marketers involved in researching various markets.

First of all, let's understand what price elasticity of demand is. This indicator characterizes the level of reaction of consumers or buyers to changes in the price of a particular product.

For example, in the market household appliances They sell a stove of a specific model. Let's assume that the price is 10,000 rubles. Let’s assume that the price of such equipment is expected to rise by 2,000 rubles. So, the price elasticity of demand shows to what level the demand for a slab of this model will change with such a price change.

When analyzing supply and demand, as well as compiling financial plan You can’t do without such an indicator, and it is an important component economic analysis market relations.

What types of elasticity of demand exist?

Price elasticity of demand describes demand in several ways, which will be discussed below.

The first type is called elastic. In economic literature, this type is often associated with so-called luxury goods. Demand for them is characterized by the fact that it will quickly decrease when the price increases and increase at the same rate when the cost of such products decreases.

You can imagine, for example, gold jewelry. How more expensive price for gold, the correspondingly more expensive the price of jewelry. Not everyone can afford expensive purchases, so when the price of jewelry goes up, they will begin to refuse to purchase them. And vice versa, the cheaper gold costs, the large quantity people will be able to buy jewelry from it.

The second type is inelastic demand. It is characterized by a market where essential goods are sold. If the price of a product changes, the demand for it will not change much. That is, almost all buyers will not be able to refuse to buy the goods they need.

Examples of such products include personal hygiene items, some food products (for example, bread, cereals, meat, etc.) and other everyday items, the consumption of which does not change depending on the income received.

Unit elasticity

The third type is demand with unit elasticity. It is characterized by the fact that when the price of a product decreases or increases, demand changes by a similar level in the direction of growth or decrease, respectively.

This price elasticity of demand is characterized by a constant level of products sold in value terms, regardless of the size of the prices set for them.

The next type is called absolutely inelastic. It is associated with the goods market, the demand in which does not depend on price. That is, whatever the price of the product, people will buy it.

For example, various medications for which there is no alternative will always be purchased. Such products are those types of essential goods that are presented on the market in only one form, and there is simply no other choice.

Typically, prices for such goods are regulated by the state in order to provide social protection and guarantees for low-income segments of the population.

The last type is perfectly elastic demand. It is characterized by the fact that consumers are willing to pay only a certain price for a product. If it changes, there is a complete rejection of such products.

Such price elasticity of demand for a product is more likely a special case than a common rule. Often it looks like this: the manufacturer sets its break-even point with the price of the product.

Often, manufacturing companies receive government payments for such goods so that such a business has at least some attractiveness. Raising the price level for such products means completely losing all buyers.

Price elasticity of demand: calculation formula

The level of demand elasticity is determined as a coefficient. Its analysis allows us to draw conclusions about the market situation.

Coefficient price elasticity demand is equal to the following formula: Kce = %Is / %Its, where:

- Kce – elasticity coefficient;

- %Is - percentage changes in volume

- %Its - percentage changes in price.

- %Is = (current volume of demand - initial volume of demand) / initial volume of demand x 100%.

- %Its = (current price - starting price) / starting price x 100%.

Based on the simplicity of the formulas, it is easy to find out what the coefficient of price elasticity of demand is equal to. But after obtaining the result, you need to correctly determine what elasticity it describes.

How to understand the coefficient values?

So, let's assume that we did the math and got certain data. We learned what the price elasticity of demand is equal to. To decipher the results, you can use the following table:

Factors of price elasticity of demand

Elasticity can be affected by many things, which, in fact, determine the essence of the market. But the following factors can be distinguished:

- Product category.

- Time.

- Substitute goods.

Let's look at each one in order.

Product category directly affects the elasticity of demand

Agree that a person will buy them regardless of whether they become more expensive or cheaper, because his life depends on it. And many more such examples can be given.

On the other hand, consider vintage wine. The higher the price, the fewer people will want to buy it. This is the essence of this factor.

The time factor also has a significant impact on the level of elasticity of demand. The longer the period of time that is considered, the more elastic the demand will be.

Effect of time on elasticity

This can be explained as follows. Imagine that you constantly buy the same sausage in a store. Do this regularly. You are satisfied with everything: the quality, composition and other characteristics of this product.

But one day you come to the same store, and the sausage has become 30% more expensive. This is an unaffordable amount for your budget. At the same time, you fundamentally do not want to buy another one, since you do not trust other manufacturers. Your demand for this product is currently inelastic.

A day passes, then a second, a third, a week and so on. Your favorite sausage is not getting cheaper, and you begin to think that you can still afford to buy it, or you will have to try a similar product from another manufacturer for a lower price. Now your demand has become more elastic - you are ready to consider different options.

On this simple example can explain the effect of time on the level of elasticity of demand.

If the product is not unique, then demand will be elastic

This statement is suitable to express the essence of the third factor.

Indeed, the more substitute products there are on the market, the more difficult it is to force the buyer to choose products from only one manufacturer at a dictated price.

Substitute products refer to similar products on the market, which may have some different properties from the main product, but, in principle, provide the same satisfaction.

For example, you love Coca-Cola. Pepsi tastes the same and is no different. If the manufacturer sharply increases the price of your favorite drink, then you can start drinking Pepsi to save money. That is, any good that can painlessly replace another good is called a substitute good.

And in such a market, it is quite difficult for a manufacturer to impose its price on consumers, because because of this, customers may go to competitors. The level of competition in markets where there is no uniformity of goods and there are many manufacturers who make similar products is, if not ideal, then with high level competition and fair prices.

The main thing is to draw the right conclusions

When analyzing any economic indicator, one should not rush and draw hasty conclusions. Once only the coefficient of price elasticity of demand has been calculated, it is impossible to try to decipher it and identify certain signs of the market.

To compile a complete market analysis, you need to calculate a similar coefficient on supply, the level of competition, government regulation, the purchasing power of consumers and many other different indicators. Only after this can one draw respectable conclusions and make various decisions regarding the management of economic activity, using the coefficient of price elasticity of demand.

And do not forget that the science of economics is only accurate at first glance. After all, a decision made today may turn out to be wrong tomorrow.

The concept and essence of elasticity of demand

Price Elasticity of Demand- an indicator calculated as the ratio of the change in the volume of demand, expressed as a percentage, to the change in price, also expressed as a percentage.Determinants of price elasticity of demand

Elastic and inelastic demand. According to the law of demand, a decrease in the price of a product increases the quantity demanded. Price elasticity of demand determines the response of the quantity demanded to changes in the price of a product. Demand for a product is said to be elastic if the quantity demanded changes significantly when the price changes. Demand is said to be inelastic if the quantity demanded changes slightly when the price changes.

Factors of demand elasticity

Price elasticity of demand is determined by a variety of economic, social and psychological factors that shape human desires. The main factors of price elasticity of demand are given below.Essential goods and luxury goods. The demand for necessities has low price elasticity, while the demand for luxury goods has high price elasticity. People are making little reduction in their consumption of everyday foods (such as bread), even if food prices increase. But rising prices in restaurants lead to a significant decrease in the use of their services. The reason is that most people view food in general as a necessity and dining out at an expensive restaurant as a luxury. Of course, what is a luxury for one person may be considered a daily necessity by another. However, most people in a given society categorize necessities and luxuries equally.

Availability of close substitute products. Goods that have close substitutes have more elastic demand. Consumers in this case have the opportunity to use one product instead of another. For example, tangerines and oranges are quite easily interchangeable. A slight increase in the price of tangerines (while the cost of oranges remains unchanged) will lead to a significant decrease in the volume of sales of tangerines. Against, salt- a product that has no close substitute, so the demand for salt is less elastic than the demand for tangerines.

Market breadth. The elasticity of demand depends on the definition of the boundaries of any market. A more narrowly defined market is also characterized by more elastic demand compared to a broadly defined market, in which it is much easier to find substitute goods. For example, food products, a broad product category, have virtually inelastic demand because they have no substitutes. Citrus fruits are a narrower product category, so they also have more elastic demand, since they are easier to replace with other fruits and berries.

Time horizon. Over long periods of time, the price elasticity of demand for goods increases. When the price of gasoline rises, the volume of demand for it decreases slightly over the course of months, but over time, people begin to use public transport more frequently and purchase more fuel-efficient cars. As a result, as prices rise over time, the demand for gasoline will decrease significantly.

Calculation of price elasticity of demand

Price elasticity of demand is calculated as the ratio of the change in volume of demand, expressed as a percentage, to the change in price, expressed as a percentage:

Let's say the price of an apple increases by 10% and you now buy 20% fewer apples. The price elasticity of demand will be:

A price elasticity of demand of 2 means that the change in quantity demanded is twice as large as the change in price.

Since the quantity demanded of a good is inversely proportional to its price, the sign of the change in quantity demanded, expressed as a percentage, is always opposite to the sign of the change in price, expressed as a percentage. For this reason, the price elasticity of demand will be a negative number. Typically, price elasticity is considered a positive number, which mathematicians call its absolute value.

Clarification of the calculation of price elasticity of demand

Arc elasticity. You can clarify the calculation of price elasticity of demand using the following formula:

In this formula, Q2 and P1 denote the quantity of a good and the price at one point on the demand curve, respectively, and Q2 and P2 denote the quantity of a good and the price at another point on the demand curve, respectively. These points are connected by an arc, which represents a segment of the demand curve. Therefore, the elasticity obtained by calculation using the above formula is called arc elasticity.

Point elasticity. If the arc of the demand curve, limited by points Q2 P1 and Q2, P2, contracts and turns into a point, then the calculated elasticity is called point elasticity.

Types of demand curves by elasticity

Types of demand curves are classified according to their elasticity.

Elastic, inelastic and neutral elastic demand. Demand is said to be elastic when the elasticity is greater than 1. That is, the percentage change in quantity of a good is relatively greater than the percentage change in price. Demand is assessed as inelastic when the elasticity is less than 1. That is, the change in quantity of a good is relatively less than the change in price. If elasticity is 1, i.e. the relative quantity of a good changes in exact accordance with changes in price, demand is characterized by unit (neutral) elasticity.

In Fig. Figure 2.11 shows three types of demand curves with different elasticities.

Rice. 2.11. Elastic (elasticity less than 1), neutral elastic (elasticity equal to 1) and elastic (elasticity greater than 1) demand

In the case of zero elasticity, demand is completely inelastic and the demand curve is vertical. With perfect elasticity of demand, the price elasticity of demand tends to infinity and the demand curves are horizontal. These extreme cases are shown in Fig. 2.12.

Total revenue and price elasticity of demand

Total revenue is the amount of money paid by buyers and received by sellers of goods, calculated as the product of the price of the goods and the quantity of goods sold. In any market, total revenue is equal to the price of the product multiplied by the quantity of the product sold: PxQ.

In Fig. 2.13, total revenue is represented by a rectangle under the demand curve, its height is equal and its length is equal to Q. The area of the rectangle, defined as PxQ, is equal to the total revenue received from this spurt. If P = 3 rubles, Q = 100, total revenue is 3 x 100 = 300 rubles.

Rice. 2.13. Total revenue - represented by the rectangle under the demand curve

The nature of the change in total revenue when the price changes depends on the price elasticity of demand. If demand is inelastic, an increase in price leads to an increase in total revenue. Let the price increase from 2 to 4 rubles with inelastic demand. This results in a decrease in quantity demanded from 100 to 80 units, as shown in Fig. 2.14.

Total revenue increases from 100 to 320 rubles. An increase in price leads to an increase in the product Px Q, since the reduction in the number of sales Q is less than the increase in P. As a result, revenue increases.

If demand is elastic, the result will be the opposite. An increase in price leads to a decrease in total revenue, as shown in Fig. 2.15. The price of the product increased from 8 to 10 rubles, the volume of demand decreases from 100 to 60 units.

Rice. 2.14. Change in total revenue when price changes:

inelastic demand

As a result, total revenue is reduced from 800 to 600 rubles. Since demand is elastic, the decrease in quantity demanded is large enough to offset the increase in price. That is, an increase in price leads to a decrease in the product PxQ, because the decrease in Q is relatively greater than the increase in P.

General rules for assessing changes in revenue. If the price elasticity of demand is less than 1, an increase in price leads to an increase in total revenue, and a decrease in price leads to a decrease in total revenue. If the price elasticity of demand is greater than 1, an increase in price leads to a decrease in total revenue, and a decrease in price leads to an increase in total revenue. When the price elasticity of demand is 1, a change in price has no effect on total revenue.

Elasticity and revenue with a linear demand curve

Demand curves are typically characterized by variable elasticity throughout their entire length. A simple example of a demand curve with variable elasticity is the straight line in Fig. 2.16. A linear demand curve has a constant slope. But the elasticity of the demand curve will not be constant. The reason is that slope is the ratio of changes in two variables, while elasticity is the ratio of relative magnitudes—changes in variables expressed as a percentage. Therefore, when low prices and high quantity demanded, the demand curve is inelastic. When prices are high and quantity demanded is small, the demand curve is elastic.

In table 2.8 shows demand data corresponding to the demand curve in Fig. 2.16 and calculations of price elasticity of demand. Changes in prices and quantity demanded are made by dividing the changes by average value adjacent values of prices and quantities of demand. Total revenue at each point on the demand curve illustrates the relationship between total revenue and elasticity. When price is 4, the elasticity of demand reaches unity and revenue reaches its maximum.

Other estimates of demand elasticity

Income Elasticity of Demand.

Income elasticity of demand is an estimate of the impact of consumer income on the volume of demand. Its value is calculated as

Normal goods. Most goods fall into the category of normal goods. The quantity demanded for normal goods and income move in the same direction; normal goods have a positive income elasticity. The income elasticities of different normal goods vary significantly. Essential goods - food - are characterized by low income elasticity, since consumers, regardless of their income, are forced to purchase at least some of them. Luxury goods such as jewelry have high income elasticity. Declining income forces consumers to abandon overly expensive goods.

Inferior goods are goods whose consumption decreases as consumer income increases. Quantity demanded and income move in different directions, so inferior goods have a negative income elasticity.

Cross price elasticity of demand

Cross price elasticity of demand shows how the quantity demanded of one good changes when the price of another good changes. It is calculated as follows:

The cross price elasticity of demand for substitute goods is positive. These products may be substitutes for each other. Therefore, if the price of one increases, the purchase of the other increases.

The cross price elasticity of demand for complementary goods—goods that are used together—will be negative. An increase in the price of one product leads to a decrease in purchases of another product.

Topic 9.

Elasticity of supply and demand

Elasticity - the degree of response of one variable in response to a change in another associated with the first quantity.

The concept of “elasticity” was introduced into economic literature A. Marshall(UK), his ideas were developed J. Hicks(Great Britain), P. Samuelson(USA), etc.

The ability of one economic variable to respond to changes in another can be illustrated by various methods, based on the chosen units of measurement. In order to unify the choice of units of measurement, the percentage measurement method is used.

A quantitative measure of elasticity can be expressed through the elasticity coefficient.

Coefficientelasticity is a numerical indicator showing the percentage change in one variable as a result of a one percent change in another variable.

Elasticity can vary from zero to infinity.

The following are distinguished: types of elasticity:

Price elasticity of demand;

Income elasticity of demand;

Price elasticity of supply;

Cross price elasticity of demand;

Point elasticity of demand;

Arc elasticity of demand;

Elasticity of the price-wage ratio;

Elasticity of technical substitution;

Straight line elasticity.

Forms of elasticity :

elastic demand (ED > 1) . A situation in which quantity demanded changes more than prices. For example, a 1% increase in price causes a decrease in quantity demanded by 4%;

Analysis of consumer behavior;

Determining the company's pricing policy;

Determining the strategy of firms and business enterprises that maximizes their profits;

CROSS PRICE ELASTICITY OF DEMAND expresses the relative change in the volume of demand for one good when the price of another good changes, all other things being equal.

There are three types cross elasticity demand by price:

· positive;

· negative;

· zero.

Positive cross price elasticity of demand refers to interchangeable goods (substitute goods). For example, butter and margarine are substitute goods; they compete in the market. An increase in the price of margarine, which makes butter cheaper relative to the new price of margarine, causes an increase in demand for butter. As a result of an increase in the demand for oil, the demand curve for it will shift to the right and its price will rise. The greater the substitutability of two goods, the greater the cross-price elasticity of demand.

Negative cross price elasticity of demand refers to complementary goods (related, complementary goods). These are goods that are shared. For example, shoes and shoe polish are complementary goods. An increase in the price of shoes causes a decrease in the demand for them, which, in turn, will reduce the demand for shoe polish. Consequently, with a negative cross elasticity of demand, as the price of one good increases, the consumption of another good decreases. The greater the complementarity of goods, the greater will be the absolute value of the negative cross price elasticity of demand.

Zero Cross price elasticity of demand refers to goods that are neither substitutable nor complementary. This type of cross price elasticity of demand shows that consumption of one good is independent of the price of another.

The values of cross price elasticity of demand can vary from “plus infinity” to “minus infinity”.

Cross price elasticity of demand is used in the implementation of antitrust policy. To prove that a particular firm is not a monopolist of a good, it must prove that the good produced by this firm has a positive cross-price elasticity of demand compared to the good of another competing firm.

An important factor determining cross-price elasticity of demand is the natural characteristics of goods and their ability to replace each other in consumption.

Knowledge of the cross price elasticity of demand can be used in planning. Let's say that natural gas prices are expected to rise, which will inevitably increase the demand for electricity, since these products are interchangeable in heating and cooking. Assuming that the long-run cross price elasticity of demand is 0.8, then a 10% increase in the price of natural gas will lead to an 8% increase in the quantity of electricity demanded.

The measure of the interchangeability of goods is expressed in the value of the cross-price elasticity of demand. If a slight increase in the price of one good causes a large increase in demand for another good, then they are close substitutes. If a slight increase in price one good causes a large reduction in the demand for anothergood, then they are close complementary goods.

CROSS ELASTIC RATIOSTI DEMAND BY PRICE- an indicator expressing the ratio of the percentage change in the volume of the demanded good to the percentage ratio of the price of another good.

Coffi The cross-price elasticity of demand is determined by the formula:

Ec=∆ Qx/∆ Py∙ Py/ Qx

The coefficient of cross price elasticity of demand can be used to characterize the interchangeability and complementarity of goods only with minor changes in prices. Large price changes will trigger the income effect, causing demand for both goods to change. For example, if the price of bread decreases by half, then the consumption of not only bread, but also other goods will probably increase. This option may be regarded as complementary benefits, which is not legal.

According to Western sources, the elasticity coefficient of butter to margarine is 0.67. Based on this, when the price of butter changes, the consumer will react with a more significant change in the demand for margarine than in the opposite case. Consequently, knowledge of the coefficient of cross price elasticity of demand makes it possible for entrepreneurs producing interchangeable goods to more or less correctly set the volume of production of one type of good with the expected change in prices for another good.

PRICE ELASTICITY OF SUPPLY- an indicator of the degree of sensitivity, the reaction of supply to changes in the price of a product.

Price elasticity of supply is calculated using the formula:

E= percentage change in quantity supplied / percentage change in price

The method for calculating the elasticity of supply is the same as the elasticity of demand, with the only difference being that the elasticity of supply is always positive, because the supply curve has an “ascending” character. Therefore, there is no need to conditionally change the sign of the elasticity of supply. Positive value The elasticity of supply is due to the fact that a higher price encourages producers to increase output.

The main factor in the elasticity of supply istime, since it allows producers to respond to changes in the price of a product.

There are three time periods:

- current period- the period of time during which producers cannot adapt to changes in the price level; short period- the period of time during which producers do not have time to fully adapt to changes in the price level;

· long period- a period of time sufficient for producers to fully adapt to price changes.

The following forms of elasticity of supply are distinguished:

· elastic supply- the quantity supplied changes by a greater percentage than the price when the elasticity is greater than one (Es> 1). This form of elasticity of supply is characteristic of a long period;

· inelastic supply- the quantity supplied changes by a smaller percentage than the price when the elasticity is less than one (Es< 1). Эта форма эластичности предложения присуща короткому периоду;

· absolutely (perfectly) elastic supply occurs when the quantity supplied varies indefinitely with a small change in price (Es = ∞). This form of elasticity of supply is characteristic of a long period, and the supply curve is strictly horizontal;

· perfectly inelastic supply occurs when the quantity supplied is zero (E = 0), that is, the quantity supplied does not change at all when the price changes. This form is characteristic of the current period, and the supply curve is strictly vertical.

It should be noted that for most industrial goods the elasticity of supply with respect to raw material prices is negative, because an increase in the price of raw materials leads to an increase in the firm's costs, which, other things being equal, causes a reduction in output.

The elasticity of supply depends on many factors:

Possibilities long-term storage and storage costs. A product that cannot be stored for a long time or is expensive to store has a low elasticity of supply;

Specifics production process. In the case when the producer of a good can either increase its output when the price rises, or produce another good when the price decreases, the supply of this good will be elastic;

Time factor. The manufacturer cannot quickly respond to price changes, since it takes a certain amount of time to hire additional

workers, purchase of means of production (when you need to increase your

start-up), or lay off some employees, make payments with a bank loan (when it is necessary to reduce output). In the short term, supply can be increased by an increase in demand (price) only through more intensive use of existing production capacities. However, such intensity can only increase market supply by a relatively small amount. Consequently, in the short run, supply is low price elastic. In the long run, entrepreneurs can increase their production capacity by expanding existing capabilities and by firms building new enterprises. Thus, in the long run, the price elasticity of supply is quite significant;

Prices of other goods, including resources. In this case we're talking about about cross elasticity of supply;

The degree of achieved use of resources: labor, material, natural. If these resources are not available, then the response of supply to elasticity is very small.

SUPPLY CURVE- a line reflecting all the ratios of the quantity of goods offered and the equilibrium Price; characterizes the supply of a good. A shift in the supply curve means a change in supply. An increase in supply corresponds to a shift in the supply curve to the right, and a decrease corresponds to a shift in the supply curve to the left.

POINT ELASTICITY- elasticity measured at one point on the supply or demand curve; is a constant everywhere along the supply and demand line.

Point elasticity is an accurate measure of the sensitivity of demand or supply to changes in prices, income, etc. Point elasticity reflects the response of demand or supply to an infinitesimal change in price, income, and other factors. Often a situation arises when it is necessary to know the elasticity in a certain section of the curve corresponding to the transition from one state to another. IN this option usually the supply or demand function is not specified.

To determine elasticity at price P, one must determine the slope of the demand curve at point A, that is, the slope of the tangent (LL) to the demand curve at this point. If the price increase (∆P) is insignificant, the volume increase (∆Q.), determined by the tangent LL, approaches the actual one. It follows from this that The point elasticity formula is presented as follows:

E= ∆ Q\∆ P∙ P\Q

If the absolute value of E is greater than one, demand will bedet elastic. If the absolute value of E is less than onetsy, but greater than zero - demand is inelastic.

ARC ELASTICITY- approximate (approximate) degree of response of demand or supply to changes in price, income and other factors.

Arc elasticity is defined as the average elasticity, or elasticity in the middle of the chord connecting two points. In reality, arc-average values of price and quantity demanded or supplied are used.

Price elasticity of demand is the ratio of the relative change in demand (Q) to the relative change in price (P).

Arc elasticity can be mathematically expressed as in this way:

E=(Q1-Q0)\(P1-P0)∙(P1+P0)\(Q1+Q0)

Where P0 - starting price;

Q0 - initial volume of demand;

P1 - new price;

Q1 - new volume of demand.

Arc elasticity of demand is used in cases with relatively large changes in prices, income and other factors.

The coefficient of arc elasticity, according to the statement R. Pindyka And D. Rubinfeld, always lies somewhere (but not always in the middle) between the two point elasticities for low and high prices.

So, for minor changes in the values under consideration, as a rule, the point elasticity formula is used, and for large changes (for example, over 5% of the initial values), the arc elasticity formula is used.

Elasticity- the degree of response of one variable in response to a change in another associated with the first quantity.

A quantitative measure of elasticity can be expressed through the elasticity coefficient.

Elasticity coefficient is a numerical indicator showing the percentage change in one variable as a result of a one percent change in another variable. Elasticity can vary from zero to infinity.

Types of elasticity. The following types of elasticity are distinguished:

- price elasticity of demand;

- income elasticity of demand;

- price elasticity of supply;

- cross price elasticity of demand;

- point elasticity of demand;

- arc elasticity of demand;

- elasticity of the price-wage ratio;

- elasticity of technical substitution;

- straight line elasticity.

Economic theory considers the elasticity of supply and demand.

Price Elasticity of Demand.

It shows the extent to which the consumer reacts to price changes.

E(p) - price elasticity of demand;

d Qd (%) - percentage change in demand;

d P(%) - percentage change in price.

E>

E< 1 - неэластичный спрос (на

предметы первой необходимости);

Elasticity of demand

The division of elasticity into these forms is quite arbitrary, since different goods have different elasticity coefficients. Thus, staple foods have low price elasticity of demand. Luxury goods, on the other hand, have higher price elasticity. Elasticity may vary depending on the time factor, on population groups, and on the availability of substitute goods.

Income elasticity of demand u.

This is a numerical parameter that shows what the consumer’s reaction is to changes in his income while prices remain unchanged.

,Where:

d Y (%) - percentage change in income

The meaning of income elasticity is closely related to the concept of normal goods and inferior goods. For normal goods, an increase in income causes an increase in demand. Since in this case income and demand change in the same direction, the income elasticity of demand is positive. On the contrary, for goods of inferior quality, an increase in income causes a decrease in demand. Income and demand move in opposite directions, so in this case the income elasticity of demand is negative. For certain groups of goods (salt, matches), demand does not increase with increasing income; elasticity is zero.

3. Cross elasticity.

It characterizes the sensitivity of demand for one product when prices for another change.

,Where:

E (k) - cross elasticity;

d Q1 (%) - percentage change in demand for one product;

d P2 (%) - percentage change in the price of another product.

Using the elasticity coefficient, the following types of cross elasticity can be determined:

a) E (k) > 0 for substitute goods;

b) E(k)< 0 для товаров-

комплементов;

c) E (k) = 0 for indifferent (independent) goods.

Elasticity of supply appears in the following main forms:

- Elastic supply is when quantity supplied changes by a greater percentage than price. This form is typical for a long period;

- inelastic supply, when quantity supplied changes by a smaller percentage than price. This form is typical for a short period;

- Absolutely elastic supply is characteristic of a long period. The supply curve is strictly horizontal;

- Absolutely inelastic supply is typical for the current period. The supply curve is strictly vertical.

Elasticity of supply of goods (by price) is the percentage relationship between the change in price and the change in supply.

One of the determining elements of the elasticity of supply of any product or service is the mobility of the factors of its production and output, i.e. the ease with which the necessary factors of production can be attracted from other industries. Second important factor- this time. As with demand, price elasticity of supply tends to increase over long time horizons. This is partly due to the mobility of resources, but also depends on the technologies used, the state of the production base, etc. Over time, the adaptation of producers to market conditions improves the market opportunity to match the output of their products to increased demand, which leads to an increase in the elasticity of supply.

The theory of elasticity of demand and supply is important practical significance. Elasticity of demand is an important factor influencing pricing policy companies. Another example of the actual use of elasticity theory is government tax policy, as well as employment policy.

Forms of elasticity. Price elasticity of demand appears in the following main forms:

E > 1 - elastic demand (for luxury goods);

E< 1 - неэластичный спрос (на предметы первой необходимости);

E = 1 - demand with unit elasticity (depends on individual choice);

E = 0 - completely inelastic demand (salt, medicines);

E is perfectly elastic demand (in a perfect market).

Price elasticity of demand. Elasticity measurement.

ANSWER

PRICE ELASTICITY OF DEMAND - an assessment of the change in the quantity of demand for a product when the price changes. More precisely, price elasticity of demand is the percentage change in quantity demanded divided by the percentage change in price.

Price elasticity of demand is a quantity used to measure the sensitivity of quantity demanded to a change in the price of a product, holding other factors affecting demand constant.

The price elasticity of demand for different products can vary significantly. The demand for basic necessities (food, shoes) is inelastic, since they are necessary for life and, despite the increase in price, it is impossible to refuse their consumption. Luxury goods, on the contrary, have a higher price elasticity.

The price elasticity of demand depends on the following factors:

Availability of substitute goods (substitutes). The more substitute goods that satisfy a similar human need, the higher the elasticity. Goods that have no substitutes (such as insulin) are inelastic;

Time to adjust to price changes. In the long run, demand tends to be more elastic because it is only over time that people are able to find more substitutes. In the short run, demand is very inelastic;

The share of the consumer budget allocated to the product. Small shares of the budget spent on the consumption of essential goods may not significantly affect their consumption when their prices rise. Such goods include, for example, toilet paper, salt, etc.

ELASTICITY MEASUREMENT. To measure elasticity, you need to determine how much demand changes when price changes.

The numerical value of the price elasticity of demand coefficient can be determined using the following formula:

where Q, D is the volume of demand measured along the demand curve; P – price of the product.

Let's assume that a 1% increase in the price of a new computer (all other things being equal) will lead to a 2% decrease in the number of computers sold annually (compared to the previous year). In this case, the price elasticity of demand will be: 2% / 1% = -2.

The price elasticity of demand is expressed as a negative number, because the law of demand assumes that for any change in price, the change in quantity demanded is the opposite. This means that if the denominator is positive, the numerator is negative, and vice versa. The ratio of two percentage changes is always negative, since the numerator and denominator have different signs.

The price elasticity of demand can decrease from zero to minus infinity. The greater the absolute value of the price elasticity of demand, the greater the price elasticity of demand. Thus, demand is more elastic at the value of E D = -5 than at E D = -1, because the number 5 acts as an absolute value for -5 and is greater than 1, i.e., greater than the absolute value of -1.

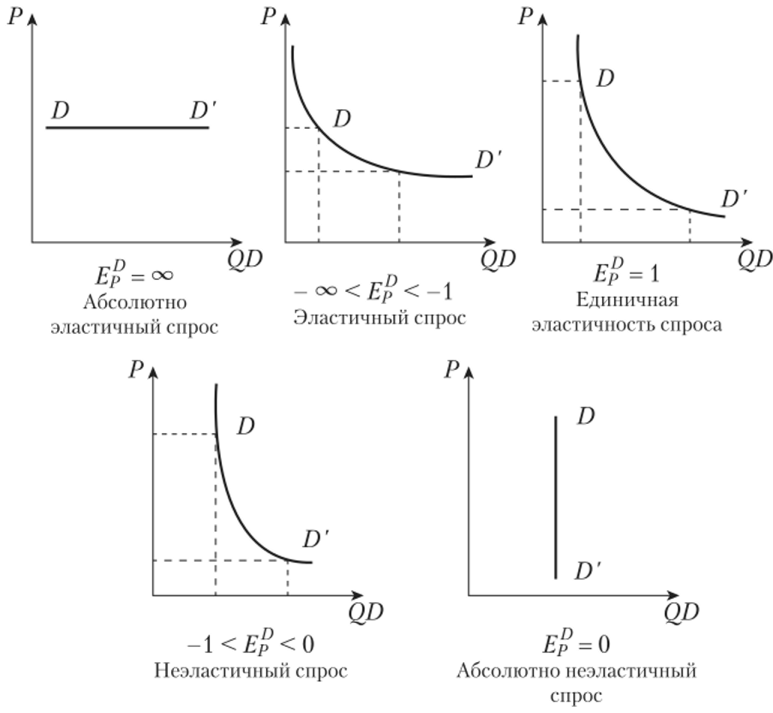

There are several forms of price elasticity of demand:

Elastic demand, if the absolute value of elasticity ranges from 1 to infinity;

Inelastic demand if the absolute value of elasticity varies from 0 to 1;

Unit elasticity if the elasticity is -1 and its absolute value is 1;

Perfectly inelastic demand if the price elasticity of demand is zero;

Perfectly elastic demand when the absolute value of elasticity is infinity.

We illustrate these forms of elasticity in Fig. 14.1, 14.2.

In Fig. Figure 14.1 shows three demand curves with different elasticities. In all cases, prices are halved, and the amount of consumer demand changes differently. In Fig. 14.1a, a halving of price causes a triple increase in demand. In Fig. 14.16 A double decrease in price leads to a double increase in demand. In Fig. 14.1c halving the price causes only a 50% increase in demand.

Rice. 14.1. Three Forms of Price Elasticity of Demand

Two extreme forms of price elasticity of demand are shown in Fig. 14.2.

Rice. 14.2. Perfectly elastic and perfectly inelastic demand

Perfectly elastic demand means that demand is infinitely elastic and a small change in price causes an infinitely large change in the quantity demanded. This demand is shown in Fig. 14.2 horizontal line.

Perfectly inelastic demand is demand whose quantity does not change at all when price changes. This demand is shown in Fig. 14.2 vertical line.

From the book MBA in 10 days. The most important programs from the world's leading business schools author Silbiger StephenPrice Elasticity of Demand In the first example, Heineken beer drinkers were willing to buy Duff beer at the asking price. After the price reduction, demand increased. If the price increased, then demand, on the contrary, would fall. The reaction or sensitivity of buyers to price changes is called

authorQuestion 40 Demand. Law of demand. Demand curve. Changes in

From book Economic theory author Vechkanova Galina RostislavovnaQuestion 48 Elasticity of demand by price and income

From the book Economic Theory author Vechkanova Galina RostislavovnaQuestion 49 Price elasticity of supply. Curve

From the book Economic Theory: Lecture Notes author Dushenkina Elena Alekseevna4. Theory of supply and demand. Elasticity The interaction of buyers and sellers in markets drives the market economy. Main elements market economy are: demand, supply, price and competition. These elements constantly interact with each other and

From the book Microeconomics author Vechkanova Galina RostislavovnaQuestion 2 Demand. Law of demand. Demand curve. Changes in demand. ANSWER REQUEST - the relationship between the price of a good and the quantity of it that buyers are willing and able to buy.B economic sense Demand is based not simply on the need or need for a particular good, but

From the book Microeconomics author Vechkanova Galina RostislavovnaQuestion 4 Interaction of supply and demand. Market equilibrium. ANSWER Above, we looked at supply and demand separately. Now we need to combine these two sides of the market. How to do it? The answer is this. The interaction of supply and demand

From the book Microeconomics author Vechkanova Galina RostislavovnaQuestion 13 Elasticity: concept, coefficient, types, forms. ANSWER Elasticity is the degree of response of one variable in response to a change in another associated with the first quantity. The concept of “elasticity” was introduced into economic literature by A. Marshall (Great Britain),

From the book Microeconomics author Vechkanova Galina RostislavovnaQuestion 15 Income elasticity of demand. Income elasticity of demand coefficient. INCOME ELASTICITY OF DEMAND is a measure of the sensitivity of demand to changes in income; reflects the relative change in demand for a good due to a change in income

From the book Microeconomics author Vechkanova Galina RostislavovnaQuestion 16 Cross price elasticity of demand. Coefficient of cross price elasticity of demand. ANSWER: CROSS PRICE ELASTICITY OF DEMAND expresses the relative change in the quantity demanded of one good when the price of another good changes, all other things being equal.

From the book Microeconomics author Vechkanova Galina RostislavovnaQuestion 17 Price elasticity of supply. Supply curve. PRICE ELASTICITY OF SUPPLY is an indicator of the degree of sensitivity, the reaction of supply to changes in the price of a product. It is calculated using the formula: The method for calculating supply elasticity is the same as

From the book Microeconomics author Vechkanova Galina RostislavovnaQuestion 18 Point and arc elasticity. POINT ELASTICITY - elasticity measured at one point on a demand or supply curve; is a constant everywhere along the supply and demand line. Point elasticity is the exact

From the book Pricing author Shevchuk Denis Alexandrovich5.1.3. Analysis and assessment of demand, its elasticity When justifying prices in the consumer goods market, it is necessary to study its relationship with demand, which determines the upper limit of the price, since its unreasonable level (high or low) is reflected in the volume of demand.

From the book Microeconomics: lecture notes author Tyurina Anna3. The concept of elasticity, elasticity of demand Demand is the volume of a good or service that an economic entity wants to include in its consumer basket at a favorable price. Elasticity is the flexibility of supply and demand in relation to

by Evans Vaughan19. Income Elasticity of Demand Tool “A man’s success is measured not by how high he climbs, but by how high he jumps when he hits the bottom,” said General George Patton, thereby emphasizing the elasticity that manifests itself in life,

From the book Key Strategic Tools by Evans Vaughan51. Price Elasticity of Demand (Marshall) Instrument On the Malay Peninsula, when asked about the best time to harvest durian, a fruit “with a hellish smell but with a divine taste,” the answer is: “When its fruit falls from the branch, the men’s sarongs ride up.”